Today I saw Tintri’s stock price take a 17% hit. Consensus among my various independent storage pals is that they’ve got two quarters of cash left, and prospects are NOT good for their ability to continue forward. Their IPO was a huge disappointment, but even if it had raised the amount of desired capital, the revenue and forward sales outlook were still both pointing to a bleak future for these guys. It’s too bad; they have some cool technology around VM performance insight in their all-flash platform.

Also, the news this week from Barron’s is that Pure Storage is shopping themselves (this comes via Summit Redstone’s Srini Nandury); IF TRUE, that’s a clear indication that they see no independent future that protects their shareholders’ value. Their revenues continue to grow, but they also have yet to produce a single dollar in profit, and it’s doubtful they will in the near future.

HP’s acquisition of Nimble is an example of how those who deploy platforms made by persistently negative-income technology firms can work out OK; HP is continuing development on the platform, and providing existing users with the comfort that their investment and their time-consuming integrations are safe. So Nimble customers can thank their lucky rabbit’s feet that the right acquirer came along.

But what if there is no HP equivalent to rescue these technology companies? Certainly Pure has built a great customer base, but will anyone want to put out the $3B-$4B that would satisfy the investors? Would Cisco risk alienating its existing partners and go it alone in the converged infrastructure space after the Whiptail fiasco? Who in their right minds would touch Tintri at this point from an acquisition perspective?

If you’ve deployed these platforms in your environment, you have some thinking to do.

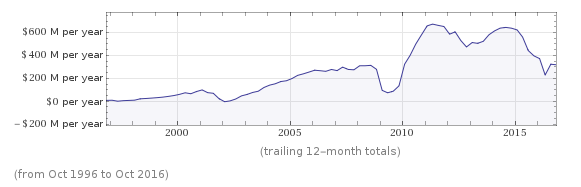

Consider this net income graph for NetApp from their IPO in 1996:

On an annual basis, Netapp has generally run at a profit from the beginning of their public life. Certainly, for the four years prior, they ran at a net loss- but their product at the time was used for specific application workloads (development/engineering) – NOT as a foundational IT component that touched every piece of the enterprise, as they do today quite well. It would have been unwise for an IT architect to consider using NetApp in 1994 to house all of their firms’ data, as the future wasn’t as certain for the technology at the time. But NetApp used their IPO in ’96 as a statement that “we’re here, we’re profitable, and we’re ready to make our lasting mark on the industry.” Which they did and continue to do.

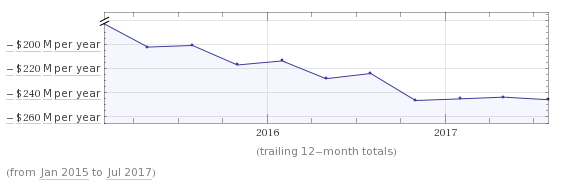

For comparison, let’s look at Pure Storage net income since it’s IPO:

It’s hard to call the right side of that chart a “turnaround”. It’s more of an equilibrium.

Now Pure Storage has some really good technology. The stuff works, it works well, and it’s relatively easy to implement and manage. However, Pure does not differentiate from the other established (and PROFITABLE) competitors in their space enough for that differentiation to create a new market that they can dominate in (they’re not alone in this; NONE of the smaller storage vendors can claim that they do, that’s the problem). As is normal for today’s Angel-to-VC-to-IPO culture, Pure used their IPO as an exit strategy for their VC’s and to raise more desperately needed cash for their money-losing growth strategy (the net income chart speaks for itself). That strategy is failing. With the news that they’re shopping, they realize this too. When prospective clients realize this, it’s really going to get difficult.

So while the tech geek in all of us LOVES new and cool technology, if you’re going to make a decision on a platform that is foundational in nature (meaning it will be the basis of your IT infrastructure and touch everybody in your firm), you’d be well advised to dig deep into the income statement, balance sheet, and cash flow of the firm making that technology, and put those stats right up there with the features/benefits, speeds and feeds. Otherwise, you may have some explaining to do later.

Bottom line: if your selected storage manufacturer is losing money, has never actually made any money, and doesn’t look like they’re going to make money anytime soon, there’s a relatively good chance you’re going to be forced into an unwelcome decision point in the near-to-medium future. Caveat emptor.